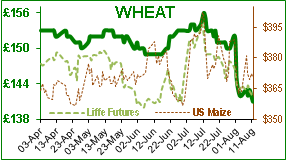

November wheat futures closed at £143.75 last Friday, and ended this week at £141.60. A month ago it was £154-ish, so we appear to be in a slow downwards trend as the EU harvest pressures the markets.

The slow downtrend is somewhat exaggerated in the accompanying wheat graph. The graphs always show the next month’s prices, and as we move from high `old crop’ prices to the lowest `new crop’ position, there appears to be a big drop. That drop is technical referring to how we record prices, rather than any exaggerated market movement.

The Matif wheat averaged about €173 for the first 6 months of this year with lows near €170; it is now trading at contract lows of €165.50. Thus US Minneapolis spring wheat drove the market skywards last month, and this month the French is driving it south. So far UK wheat is maintaining its €10/t discount to the Matif, so is now valued at €155.70. There had been some concerns about the quality and quantity of wheat in Germany, Poland and the Baltics however the USDA put Russian wheat production at a record 77.5mt which dampened any enthusiasm for price rises. Both the yield and production of the dreaded US spring wheat were reduced as expected but slightly offset by better winter wheat estimates so that total US wheat production is expected to be 47.3mt (46.6mt expected, 62.9mt last year). The wet weather has not helped the milling quality of UK wheat, and feedmillers have been offered parcels as feedwheat which have 15% protein but because it will not make the Hagberg specification (gluten elasticity measurement!) it is down-graded to feed wheat.

The USDA pulled some rabbits out of its hat this week, surprising the markets with much higher yields for maize at 169.5b/a (166.2 expected) and soya at 49.4b/a (47.39 expected). The funds sold both commodities, consequently both maize and soya prices fell; in the UK soya prices fell by about £3/t to £275 spot ex-port, and £283 for Nov/Apr on the same basis. The US soya ending stocks for 2016-17 were put at 370mb (399mb expected), and for 2017-18 were 475mb (433mb expected); which are comfortable levels. World soya production was put at 351mt for 2016-17 and 347mt for 2017-18 with world ending stocks for 2016-17 estimated at 97mt (94.4mt expected), and the 2017-18 ending stocks estimated at 98mt (92mt expected). The 2017-18 soya ending stocks have been increased by 4mt in the space of a month.

Currency, as ever, remains a wild card; as does the US president (small ‘p’) with his ‘Fire and fury’ remarks which have unsettled the world. Or is it a ploy, with US diplomats playing the good cop, and a madman the bad cop? Consequently, the Volatility Index, the VIX, hit a high of 16.8 in the year to date.

This week is the 10th anniversary of what has been seen as the start of the last financial crisis when BNP Paribas realised that nobody wanted to buy their junk mortgage bonds. Much belt tightening followed. 10 years on some people are still looking for extra income – but had you thought of hen racing? I do not think that this is something for broiler birds – their muscles are not really in their legs, and I am sure free range laying birds are faster. Would you enter yours?