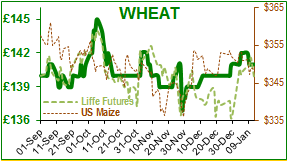

UK wheat prices spent most of the week on a slight upwards trend. The May futures closed at £141.50/t last Friday, and hit £143.00/t on Wednesday yet closed the week at £141.00/t. Demand for UK spot wheat is good and there is more than sufficient availability here in the South, so selling activity ex farm may increase now that the holidays are behind us.

The haulage of wheat from the South to the North continues, with the grain trade swapping horror stories of hauling wheat 200 miles between Christmas and New Year, only to find that the destination mill was full! European wheat prices also rose this week until the € fell for three successive days at the end of the week, then Matif wheat dropped from Tuesday’s high of €161.50 to €158.50/t on Friday.

US wheat has traded sideways for the past week, but fireworks could follow the USDA report which is released at 5pm (UK time) today. The funds are about 17Mln T short (sold) of wheat (as of 2nd January) having reduced their positions from 20Mln T (as of 26th December), thus any hint that the harvest may be reduced due to winterkill or drought might cause a fund flight to safety. About 55% of the US is currently categorised as being in drought, technically between D0 (abnormally dry) and D3 (extreme drought); traders will be watching carefully. The USDA are not expected to make large changes to US wheat stocks, Russia continues to dominate world exports, it is clear that the opportunity for the US to export this year is diminished. With an over-abundance of global wheat and projections of a near 13Mln T increase in Russian exports (40% more than last year) the US market share to world trade has fallen. US wheat sales are running at only 74% of USDA’s forecast, which equates to an export requirement of 331,000T/week to achieve the original forecast. In terms of maize, the funds are about 25Mln T short, thus any reduction in harvest estimates could start a rout.

In the physical world a new US tax law allows farmers to claim a 20% deduction on all payments received on sales of maize wheat and soya to cooperatives. There is no such provision for farmers who happen to sell to privately-owned companies such as ADM, Cargill and Bunge – active processors, exporters and suppliers to the bioethanol trade – who are understandably concerned, as they seem unlikely to be able to compete with the co-ops. Farmers are already trying to relocate their agricultural crops stored in private elevators to a cooperative. This type of market distortion is likely to cause major disruption to the US and global supply chains.

As previously reported, the USDA has negotiated a new phytosanitary procedure to comply with import requirements to China, by reducing the acceptable level of foreign material from 2% to 1% from Jan 1st. China complained it was receiving too much soil and weed seeds in US consignments and threatened quarantine procedures. As a first step the US Animal Health and Plant Inspection Service (APHIS) will label most soya shipments 'This consignment exceeds 1% foreign material'. Reuters suggest that had this new rule been implemented a year ago, then more than 50% of US soya shipped to China in 2017 would have been so labelled. US soya exports are about 7Mln T behind last year, which partly explains why the funds are about 12Mln T short of soya; that and the fact that US soya ending stocks are expected to be a comfortable 445Mln Bushels this year (301Mln B last year, and 197Mln B in 2015-16). Brazil expects to produce 110Mln T of soya this year, and increase of 1Mln T from last month’s estimate, and only 3.5Mln T less than last year’s record. In Argentina about 90% of its soya crop has been planted, but it is still too dry in the North.

Once in a blue moon:

Snow in the Sahara? For only the third time in 40 years it snowed this week, up to 15 inches deep at Ain Sefra near the Atlas Mountains in Algeria. Not a toboggan in sight.

There is a song in there somewhere: