Currencies

The £ has kept relatively stable, up slightly against the $. The outcome of the Bank of England Monetary Policy Committee this week to raise interest rates by a further 0.25% up to 0.5% was seen as positive by the markets.

Interestingly in the same week, the European Bank Monetary Policy Committee decided against any policy changes because they felt that inflation was coming back in line to meet their 2% target, whilst the US has just released the highest inflation figure in 40 years of 7%.

Wheat

Wheat is currently over all up on the week although trading back down today. The Russian and Ukraine story continues to bubble in the background with reports now suggesting any form of invasion will not go ahead until after the Winter Olympics?

China have also now confirmed that they have signed a trade policy which opens imports from across Russia and not just the 7 specified areas under the previous agreement which would be seen as a boost the Russian economy.

If Russia do decide to go ahead with any form of invasion, then at the moment it is being suggested any economic sanctions against Russia will exclude food so in theory, wheat trade can continue as normal but we have seen before that Russia will manipulate their wheat exports with tariffs or caps and the rest of the world is reliant on their wheat exports this season.

Looking ahead to 2022, plantings are very much all about re building stocks and although early indications are not ground breaking, they would be enough to pull us out of the current situation. US is looking slightly dry across central regions which will need to be kept an eye on. In the UK the Vivergo ethanol plant has reopened this week which could push some of those northern feed wheat premiums higher.

USDA report this week was fairly benign for wheat with end stock slightly lower than trade expectations, but nothing of note. Unsurprisingly though corn numbers were cut but only by 1 MlnT which over all left end stocks higher than expected.

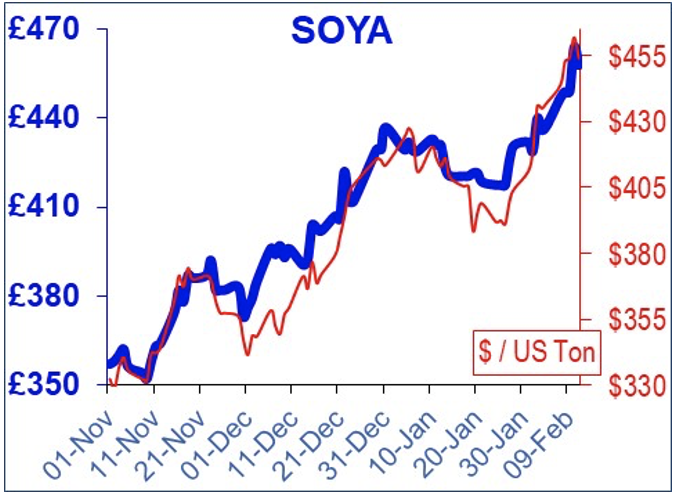

Soya

Soya markets did react more to the USDA report which cut global production by 8.7 MlnT to 363.9 MlnT, although this was still lighter than the market had anticipated. There has now been no reportable rain across Argentina or Brazil for 14 days.

The other bullish factor is that China are not as well covered as previously thought and are buying in large quantities.

The truth is that reports are varying by over 10 MlnT worth of production now for South America which means, we do not know where we really are. Only the progression of harvest and yield data will make the long term picture clear.

And Finally…

Happy Valentine’s Day!

Regards,

Kay Johnson & Martin Humphrey