Currencies

The £ continues to hold steady with little to drive it either way at the moment. The CPI data released this week remained at 5.4%, the same as December’s figures.

The main story continues to be between Russia and Ukraine and what impact that would have to markets should it escalate.

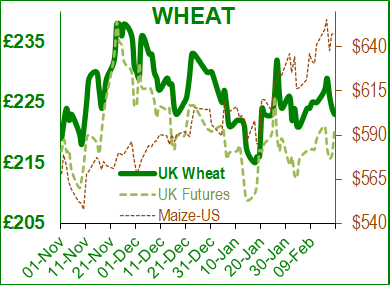

Wheat

As mentioned last week, the USDA report had very little impact on prices and this week prices have continued to move lower, albeit remaining volatile within a range.

Russia and Ukraine continues to be the main story for wheat so there is now a risk premium factored into prices which could mean if tensions de escalate, prices could move lower.

Having said that, prices could also move the other way if the opposite happens. NATO have said that any sanctions against Russia would exclude food, but when the rest of the world is reliant on Russia for wheat and oilseeds, it is a possibility that Russia would turn the tap off the other way.

Technically, May futures have almost a compression type pattern at the moment which can be a signal of an upwards move. We are also starting to see a split with an additional premium being put on feed wheat in the north of the UK to cover the anticipated demand from the Vivergo ethanol plant which has now re opened.

For new crop, looking at the discount of barley against wheat, currently it does not look like that will feature in poultry feed diets this season, switching more demand to wheat. Crops are still looking good despite the lower levels of fertiliser being applied but it is still early days!

Soya

Soya continues to be led by weather with little rain falling across South America. China have also been bad buying which tends to lead the market.

Revised estimates now stand at 132.9 MlnT for Brazil and 44.2 MlnT for Argentina which is still not disastrous figures so it feels that prices are perhaps too over done?

The truth is that reports are varying by over 10 MlnT worth of production now for South America which means, we do not know where we really are. Only the progression of harvest and yield data will make the long term picture clear.

And Finally…

Regards,

Kay Johnson & Martin Humphrey