Currencies

The £ has steadied to last week’s levels of £/$1.30 and £/€1.18 with the ongoing concerns over cost of living increases which are becoming very real now.

The Bank of England MPC agreed to raise interest rates to 0.75% as expected this week which will help bring inflation back under control which is currently at a 30 year high.

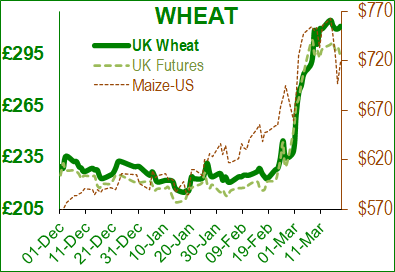

Wheat

Wheat markets remain extremely volatile although they did take a breath and gave back some of their monumental gains. This was driven more by profit taking as wheat markets are so heavily invested in by fund money at the moment. Worryingly, UK wheat is still competitive for export, tracking circa £40 under Matiff meaning that there has been bids for wheat between £7-12 over futures.

The Supply and Demand figures of UK wheat show the we are likely to be in deficit by the end of the season, and are already in deficit in some areas of the country. It does seem mad that we can currently export wheat. The inevitable outcome, is that those who have not committed to buying their wheat this season, will have to buy it back at the higher price on the continent and pay to import it – so even more expensive than we are now! Mad!!

Looking at factors outside of Ukraine, dryness across US and Canada is beginning to draw attention but reports in Europe and the UK for new crop is looking remarkably positive and it would appear that the fertiliser issue may not be as much if a factor this season as first thought although with the current situation, it will hit next season. There have been comments made that with the price of inputs, farmers need over £220 to break even, and currently Nov 23 futures are sat at £211.

Soya

Soya continues to be largely led by veg oil markets with reports that Argentina has now paused the registration for new soya oil exports and Indonesia has now said that 30% of its stock due for export must now be sold domestically to help curb inflation.

The figures in Argentina and Brazil are now looking around 43 Mlnt and 127 MlnT respectively which are still not disastrous figures but there will be more pressure now with the potential drop in other oilseed products from the Black Sea.

Organic

With a high proportion of organic raw materials coming from the Black Sea regions, there has been questions raised over the supply chain and if material will be available. We have assurances from our suppliers that material is being stored in large quantities to fulfil existing contracts in the UK already as there was time to prepare. Proteins which largely come from India and China are not affected so their shipping programmes remain the same.

The cost of storage and the limited amount of supply though, even before the Ukraine war, has meant that prices have reached new highs with organic wheat trading circa £500 per tonne now. There will be very significant rises over the coming months which we are doing all we can to communicate to packers and supermarket suppliers.

As we have said before, we understand that this is an extremely concerning time for our customers and we would encourage you to speak to your Sales Representatives to ensure you are getting the maximum performance out of your flocks or if you wish to speak about the raw material markets in more detail, our Procurement and Formulations Manager, Kay Johnson is also available.

Regards,

Kay Johnson & Martin Humphrey