Currencies

We have seen a surprise jump in the £/$ rate up to 1.38 this week with the Bank of England suggesting they may pull forward their timelines to raise interest rates.

However, that comes with a caveat and with high fuel rises and Covid cases increasing going into the winter, if the bank of England reverse any decisions they do follow through with, then this would be seen as serious for the £’s value. Against the €, it has raised to 1.19, which almost testing one year highs.

Wheat

With the November wheat futures contracts now almost impossible to secure, the market has shifted this week to begin pricing off the May futures which has made it a bit of an odd week while we transition.

The long term view for wheat is still very much bullish with tight supply and concern that the European export pace certainly is too fast to sustain itself and now that the UK has had its 2021 harvest classified at 14 MlnT, it raises questions whether we have over committed to exports. Certainly in the North of England, millers are beginning to import German milling wheat.

The market does however feel as though it is reaching that limit now where it will begin to impact demand. Egypt this week have cancelled shipments for November delivery and with maize now continuing to come under pressure, there will be a good percentage which will switch into this for animal feed from wheat.

For the UK, we are still probably £40-50 away from that but it would be a spread worth watching! With a seemingly bumper US crop and good plantings in South America, the maize price is falling and the wheat does not seem to be able to hang onto any bearish news long enough to sustain a downward trend.

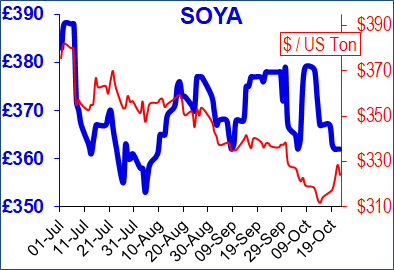

Soya

Soya prices have continued to trend downwards with increased US supply as harvest progresses. There has been a rise in Chinese buying but this will need to be sustained to turn the current trend around.

Chicago levels are currently at their lowest since March and with continued optimism going into the South American planting season, soya is probably one of the few commodities that looks positive!

Organic Markets

Organic grain markets continue to push higher with real concerns over whether there will be adequate supply for the entire season.

The protein situation seems to be switching from favouring Chinese material back to India. China has no freight available and have withdrawn from the market for new sales. There are still concerns over whether or not they will fulfil existing contracts.

The Indian harvest is now underway and early report are that the crop looks good but offers are still limited. The premium for Indian material over Chinese is beginning to narrow back down to a more recognised figure, but those sales prices are still historically high. Q1 prices remain over £1000 per tonne, but for Q2 we are seeing around a £50 discount.

And Finally…

New images surface of exotic shipments from across the world which arrived in London during the 1920’s and 1930’s.

New images which are currently being displayed in Docklands museum in London, show the types of unusual products which were passing through the London ports during this period of global discovery.

The images capture unusual items such as huge Mediterranean sponges, lizards and even a pea shooter. The black and white images also captures the customs officials and port workers of this period who were proud to be working in what was classed as the best port facilities in the world. The collection also shows tea samplers in London’s Whitechapel testing the latest shipments.

Regards,

Kay Johnson & Martin Humphrey