Currencies

Currency continues in that same small one-point range, losing slightly against the $ this week despite the positive UK jobs data which were released. Comments from US congress that their post Covid recovery is happening quicker than they anticipated, coupled with some popular decisions from Biden, particularly around the Green Fuel Mandate, have helped strengthen the $.

Wheat

Wheat has seen a mixed week, continuing trending lower before recovering slightly yet still ending the week lower. The old crop is falling faster than the new crop, which means we are starting to see that inverse now collapse with the gap narrowing down to around £30 per tonne.

Globally, the markets have eased on both increased carryout figures and fund money now looking to exit the market before contracts become physical. It is important to remember that although the global wheat stocks are up, almost half of that is owned by China so there is no way of knowing if that wheat will ever become available to the market. The general consensus as well is that many people will chose to stay, holidaying in the UK which, which will increase the demand from the hospitality sector when it reopens, which would be supportive to old crop prices as our balance sheet remains the tightest in Europe.

Looking at new crop, prices have almost become stagnant waiting for more details on emerging crops. France did come out this week and increase their estimates to 5.67t/ha against their average of 5.47 t/ha but there is still concern in some parts of Russia that winter snow cover has begun to melt but they are still seeing cold snaps which could cause some damage. The UK is still waiting to hear from AHDB what their expectations are.

Soya

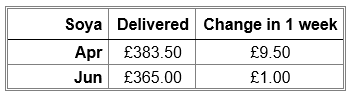

Soya, like wheat, has seen a mixed week with prices moving lower as the Brazilian story runs out of steam and harvest progresses to plan. China has now fully switched from buying US material to South American, which has eased pressure on the old crop carryout figure. The market has now turned and is seeing over spill support from the oil complex. Biden’s announcement of the Green Fuel Mandate was understandably supportive for the veg oil markets, but as it has come at a time when production figures for palm oil are still low after a difficult winter and the availability of rapeseed and sunflower continues to be lower than it has historically, it has proven very supportive for soya meal and beans.

Looking further ahead though, US farmers are expected to plant 90 Mln Acres this coming season, up from there previous record of 84 Mln, which should be long term bearish to beans, subject to Chinese demand.

And Finally…

A cargo ship the same length as the Empire State Building continues to block the famous Suez Canal

The cargo ship, the Ever Green, one of the world’s largest ships, has been stuck sideways in the canal for several days with salvage experts warning that it could take weeks to move the stricken vessel.

It is thought that there are now over 200 vessels impacted by the block, carrying goods worth an estimated $29 billion! Vessels not caught in the blockade can divert around the Cape of Good Hope but that will add around 10 days to their sailing time which adds considerable costs. On a normal day, around $9.5 billion worth of goods pass through the canal, the most valuable shipping route in the world.

This is already beginning to affect the sentiment for certain raw materials that are used in animal feeds that reach Europe via the Suez Canal.

The vessel is believed to have blown off course during strong winds, something which has happened to it before because of its sheer scale. The best chance of moving the vessel will be on Monday when the tide is at its highest so watch this space…

Of course, there is an alternative explanation as to how the Evergreen became ever-so-stuck:

Regards,

Kay Johnson & Martin Humphrey