Ukraine are now 9 days into a war and a situation which nobody would have dared to predict would happen. For the first time in over 30 years, there is a real threat to the global balance of peace and with our ever-increasing reliance on intertwined, international trade, a genuine threat to our food and gas supply chains.

At the time of writing, Ukraine is still valiantly holding back Russian troops from key cities, including Kyiv, although many of the strategic port cities have sadly been heavily bombed and appear to be largely in Russian control. Whichever way you look at it, the Ukrainian people have ensured that this has not been the simple, swift switch of power which Putin had anticipated.

Ukraine, in its own right, is one of the most commodity rich countries in the world. They are the biggest in Europe and one of the biggest globally for materials such as uranium ore, titanium, manganese, mercury and iron ore. They rank the fourth biggest in the world by total value of its natural resources.

In terms of agriculture, Ukraine is home to 25% of the world’s ‘black soil’, mineral rich soil that helps to make it one of the biggest producers and exporters of barley, sunflower, corn, wheat and potatoes. To support this, they also have three deep water shipping facilities strategically placed across the Southern coast, something which Russia lacks and it is believed these facilities was one of the reasons for Putin’s invasion.

Currencies

Looking firstly at currency, the conflict does not seem to have impacted the $/£ or €/£ exchange rate. Both these rates have been very range bound since Brexit, but on the long term trend, are already historically low, therefore have little range to react in.

If anything, the interest rate hikes believed to continue through 2022 should strengthen the £, albeit nowhere near the pre Brexit levels of nearly $2 to £1.

For Russia however, the wave of economic sanctions placed on them, from across the world, including removing Russian banks for the SWIFT system (international payment system), has effectively cut them off, and sunk the value of the Russian Rubel to less than 1 cent against the $.

In an attempt to counter this and encourage Russians to keep their money in the banks, (very much needed to fund the war chest), Putin raised interest rates from 9% to 20%. This seems to have caused more panic and encouraged a run on the banks and queues to withdraw cash from the banking system.

Wheat

Wheat, being one of the largest raw material export from both Russia and Ukraine, has seen in-comprehendible highs of close to £287 on May futures and has swung in waves of changes in £20+ movements.

Despite the pledge that food sources are not weaponised during conflict, with Russia out of the SWIFT system, all international trade has effectively stopped and that means taking close to 24 MlnT of wheat out of the global markets, on a year where stock levels have been delicate at best.

The remainder of the Black Sea (Romania, Ukraine etc), is all out of bounds for trading as well through fear of Russian torpedo strikes, taking yet more volume out of the market.

Worryingly, despite China appearing to distance themselves from Putin’s actions, they have signed a trade deal this week supporting ‘unconditional import of wheat, barley and corn from Black Sea areas’. This could give Putin a way to trade still, but in a convoluted way which will be difficult for the market to gauge.

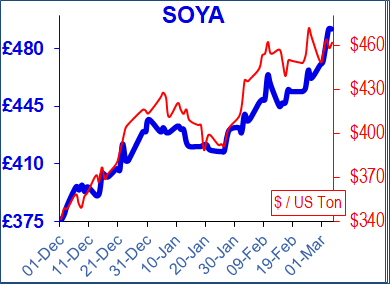

Soya

The soya market, despite not being drawn from the Black Sea regions, has felt spillover support from the threat to other oilseeds, mainly sunflower. The market had been waiting in anticipation of the South American soya harvest, which although down from its original figures, still looked healthy enough that the market would likely fall once yield data began to pull through.

Now we are in a situation where summer soya is around £480 per tonne in the UK, £40 a tonne higher than you would have paid 10 days ago and £180 above a normal price.

Ukraine is the biggest producer of sunflower in the world, and heavily manipulates the veg oil market. All sales from the region have currently stopped, placing all reliance on the small Argentinian crop.

UK stores have a few months supply as stock, but the longer this war continues, the more question marks we will have over if contracts will come off or if force majeure is called on them. Currently the price of sunflower in the UK is close to £370 per tonne, £170 per tonne over what would be considered a ‘normal’ value.

Organic

The UK imports circa 107,000 tonnes of organic wheat each year, all of which comes from the Black Sea and the Baltic States. The largest exporter to the UK is Romania, with Russia and Ukraine not far behind. The issue as we have said from some time is that harvest last year was not great for volume, and with the low premiums the previous season, most had sold out of their stocks by selling as conventional, therefore reducing any carryout for this current season. Ultimately this means that none of the other Black Sea countries have sufficient stock to plug the gap left by Russia and Ukraine.

For now, UK shippers have had time to plan for a worse case scenario, and we have stock in the UK to see us through old crop but, as with oilseeds, the longer this continues, the more questions we will be asking about new crop. Will we be able to trade with Russia? What do the crops in Ukraine look like as part of a war zone? Are there any shipping facilities left in Ukraine to ship material if there is even a harvest?

Organic protein is less of a concern because the origin for soya and sunflower here is mostly China, India and Turkey, although the Turkish material is likely to be of Ukrainian origin. Proteins though have been at historic highs because of supply chain issue, container freight etc and these situations are unlikely to ease in the near by certainly, but perhaps not even for new crop November/December time.

Energy and Oil

It has been well documented that the rest of the world is heavily reliant on Russian gas and oil. This forced switch because of sanctions has pushed prices to a record high with crude oil currently trading at $117 a barrel, breaking the previous high of $113 back in 2014.

For us in the UK this means higher energy prices, adding another pressure on poultry production, but in terms of feed, fuel rates have been reported as having the potential to rise 20 pence per litre in the coming weeks.

What does this mean for feed prices?

At the time of writing, the market swings would suggest that compared to a week ago on replacement, conventional prices are likely to rise around £40 per tonne, with organic £40-50. These are significant price rises and whilst we have some raw material cover, feed compounders never have enough cover on rising markets like this, and are not in a position to mitigate such huge movements on worldwide commodity markets.

Just in case you thought it was just our markets that have risen sharply in the last week, Bloomberg has looked at many different commodity types, and they are all up. The trouble is, our key commodity; wheat is up so much more:

Now more than ever, our Poultry Specialists are ready to work with you to ensure maximum efficiency and performance for your birds. If you have any concerns or would like to speak more about the raw material market, our Procurement Manager, Kayleigh Johnson is on hand.

And Finally…

Before Volodymyr Zelensky was Ukraine’s President, he was the voice of Paddington Bear!

Regards,

Kay Johnson & Martin Humphrey